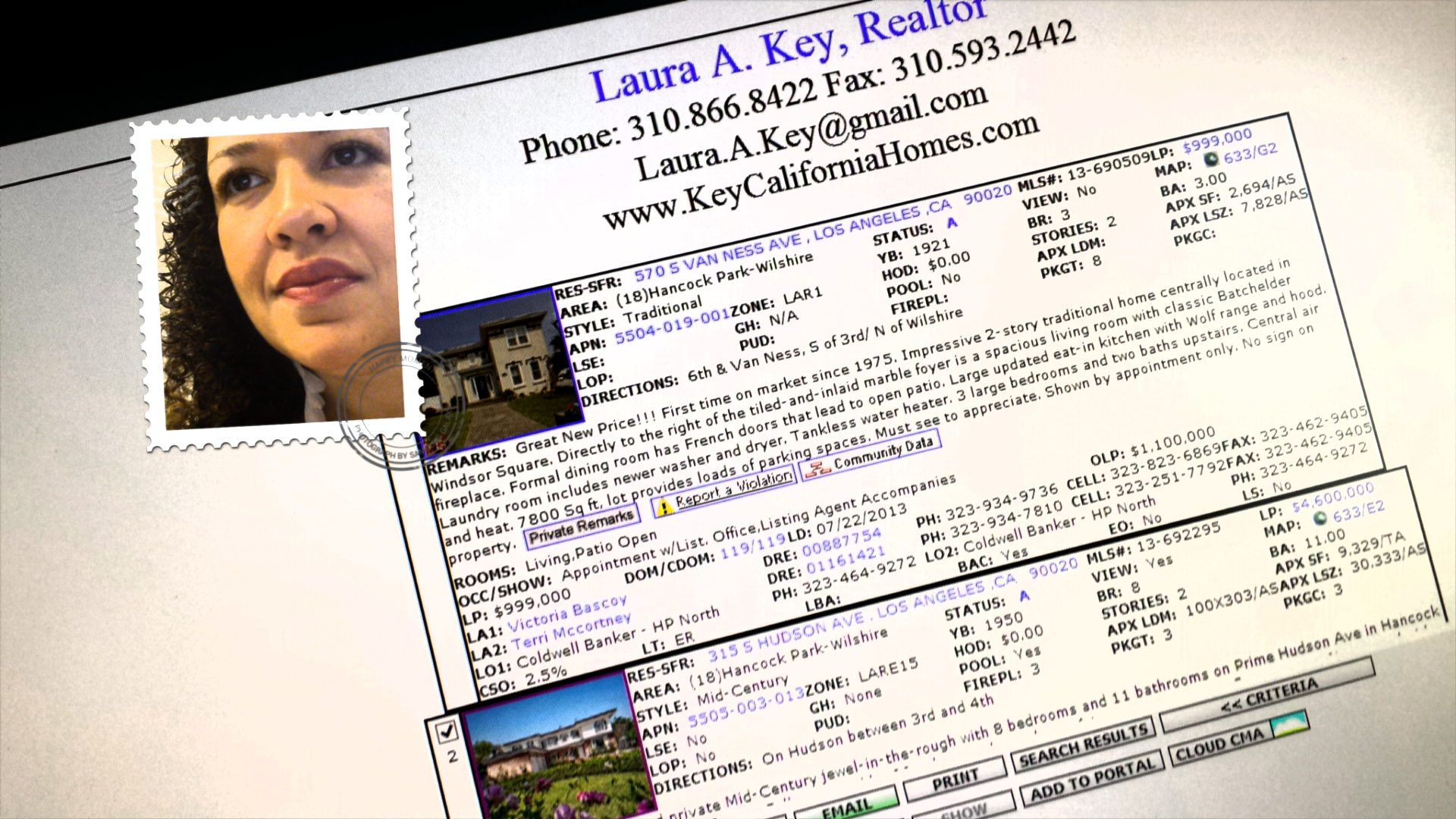

BLOG

Hard at Work In Real Estate

Looking for A New Home? Text LKHOMES to 87778 to get instant free access to the MLS! Or Call me at 310.866.8422

Homes are turning over quickly in Los Angeles! Let me work hard for you!

California Real Estate, Los Angeles Homes, Homes for Sale, Larchmont Homes for Sale, Hancock Park Homes for Sale, Windsor Square Homes for Sale, West Hollywood Homes for Sale, Koreatown Homes for Sale, Realty Goddess, Top Los Angeles Real Estate Agent, Real Estate Agent, Realtor, MLS, Home Search

Higher Home Prices Cool Buying Frenzy

Is all this frenzy creating a mini-housing bubble? What are your thoughts on this housing market? Laura Key 310.866.8422

The recent rise in home prices has more investors concerned that it will be increasingly difficult to turn a profit from their rental investments. Nearly half of U.S. real estate investors say they expect to purchase fewer rental homes in the next year, according to a recent survey conducted by polling firm ORC International.

Just 10 months ago, the percentage of investors who said they intend to buy fewer homes stood at 30 percent—compared to 48 percent today. Only about 20 percent of the investors surveyed say they plan to buy more homes in the next year—a drop from the 39 percent who reported they intend to buy more homes last August.

More than half of the investors surveyed who own rental properties say they plan to hold them for at least five years or more, and 33 percent plan to hold them for 10 years or more.

“Higher prices are reducing returns on investment and investors are responding by cutting back on their purchasing plans until conditions sort out,” says Chris Clothier, a partner in MemphisInvest.com and Premier Property Management Group. “Fewer foreclosures, rising property values, and competition from hedge funds are making it tough to find good ideals on distressed sales. On the other hand, investors are planning to hold onto their rental properties for at least eight to 10 years and realize the benefits of rising rents and low vacancy rates. Cash flow is much more important than appreciation.”

Source: ORC International

Laura Key, CBS News, Buyer's Agent, Selling Agent,

Thinking of Selling? I have buyers who are pre-approved and ready! They are looking in several areas of Los Angeles county!

When It Comes to Wood Floors, Choose Wisely

Rich wood flooring can spell instant warmth and patina in a home. Here’s an overview that can help you evaluate if wood floors are right for you! Laura Key 310.866.8422

Just as with ties and hem lengths, wood flooring styles change. Colors get darker or lighter; planks get narrower or wider; woods with more or less grain show swings in popularity; softer or harder species gain or lose fans; and the wood itself may be older, newer, or even pre-engineered with a top layer or veneer-glued to a substrate to decrease expansion and contraction from moisture.

Here are key categories for consideration:

Solid Plank

This is what some refer to as “real” wood because the wood usually ranges from three-eighths to three-quarters of an inch in total thickness to permit refinishing and sanding. Thicker floors have a thicker wear layer to allow for more frequent refinishing and sanding, so they can withstand decades of use, says architect Julie Hacker of Stuart Cohen and Julie Hacker Architects. It also can be stained, come from different species of tree, and be sold in numerous widths and lengths:

- Width and length: Designer Steven Gurowitz, owner of Interiors by Steven G., is among those who prefers solid flooring for many installations because of its rich, warm look. Like other design professionals, he’s seeing greater interest in boards wider than the once-standard 2 ¾ to 3 ¾ inches — typically 5 to 6 inches now but even beyond 10 inches. And he’s also seeing corresponding interest in longer lengths, depending on the species. Width and length should be in proportion. “The wider a board gets, the longer the planks need to be, too, and in proportion,” says Chris Sy, vice president with Carlisle Wide Plank Floors. These oversized dimensions reflect the same trend toward bigger stone and ceramic slabs. The downside is greater cost.

- Palette: Gurowitz and others are also hearing more requests for darker hues among clients in the northeastern United States, while those in the South and West still gravitate toward lighter colors. But Sprigg Lynn, on the board of the National Wood Flooring Association and with Universal Floors, says the hottest trend is toward a gray or driftwood. Handscraped, antique boards that look aged and have texture, sometimes beveled edges, are also become more popular, even in modern interiors, though they may cost much more.

- Species and price: Depending on the preference of the stain color, Gurowitz favors mostly mahogany, hickory, walnut, oak, and pine boards. Oak may be the industry’s bread and butter because of the ease of staining it and a relatively low price point. A basic 2 ¼-inch red oak might, for instance, run $6.50 a square foot while a 2 ¼-inch red oak that’s rift and quartered might sell for a slightly higher $8.50 a square foot.

- Maintenance: How much care home owners want to invest in their floors should also factor in their decision. Pine is quite soft and will show more wear than a harder wood like mahogany or walnut, but it’s less expensive. In certain regions such as the South, pine comes in a harder version known as heart pine that’s popular, says Georgia-based designer Mary Lafevers of Inscape Design Studio. Home owners should understand the different choices because they affect how often they need to refinish the wood, which could be every four to five years, says Susan Brunstrum of Sweet Peas Design-Inspired Interior. Also, Sy says that solid planks can be installed over radiant heating, but they demand expert installation.

Engineered Wood

Also referred to as prefabricated wood, this genre has become popular because the top layer or veneer is glued to wood beneath to reduce expansion and contraction that happens with solid boards due to climatic effects, says Sy, whose firm sells both types. He recommends engineered, depending on the amount of humidity. If home owners go with a prefabricated floor, he advises a veneer of at least one-quarter inch. “If it’s too thin, you won’t have enough surface to sand,” he says. And he suggests a thick enough substrate for a stable underlayment that won’t move as moisture levels in a home shift.

His company’s offerings include an 11-ply marine-grade birch. The myth that engineered boards only come prestained is untrue. “They can be bought unfinished,” he says. Engineered boards are also a good choice for home owners planning to age in place, since there are fewer gaps between boards for a stable surface, says Aaron D. Murphy, an architect with ADM Architecture Inc. and a certified Aging in Place specialist with the National Association of Home Builders.

Reclaimed Wood

Typically defined as recycled wood — perhaps from an old barn or factory — reclaimed wood has gained fans because of its aged, imperfect patina and sustainability; you’re reusing something rather than cutting down more trees. Though less plentiful and more expensive because of the time required to locate and renew samples, it offers a solid surface underfoot since it’s from old-growth trees, says Lynn. Some companies have come to specialize in rescuing logs that have been underwater for decades, even a century. West Branch Heritage Timber,for instance, removes “forgotten” native pine and spruce from swamps, cuts them to desired widths and lengths, and lays them atop ½-inch birch to combine the best of engineered and reclaimed. “The advantage is that it can be resanded after wear since it’s thicker than most prefabricated floors, can be laid atop radiant mats, and doesn’t include toxins,” Managing Partner Tom Shafer says. A downside is a higher price of about $12 to $17 a square foot.

Porcelain “Wood”

A new competitor that closely resembles wood, Gurowitz says porcelain wood offers advantages: indestructibility, varied colors, “graining” that mimics old wood, wide and long lengths, quickness in installation, and no maintenance. “You can spill red wine on it and nothing happens; if there’s a leak in an apartment above, it won’t be destroyed,” he says. Average prices run an affordable $3.50 to $8 a square foot. The biggest downside? It doesn’t feel like wood since it’s colder to the touch, Lynn says.

Bottom Line

When home owners are making a choice or comparing floors, Sy suggests they ask these questions:

1. Do you want engineered or solid-based floors, depending on your home’s conditions?

2. Do you want a floor with more natural character, or less?

3. What board width do you want?

4. How critical is length to you in reducing the overall number of seams?

5. What color range do you want — light, medium, or dark?

6. Do you want more aggressive graining like oak or a mellower grain like walnut?

7. Do you want flooring prefinished or unfinished?

8. How thick is the wear layer in the floor you’re considering, which will affect your ability to refinish it over time?

9. What type of finish are you going to use? Can it be refinished and, if so, how?

10. For wider planks that provide greater stability: Where is the wood coming from, how is it dried, what is its moisture content, and what type of substrate is used in the engineered platform?

Thinking of selling your home? A little investment can increase your resale value! Call me for a personal consultation! Laura Key 310.866.8422

What To Ask When Looking At Potential Homes

Buying a house can be an intimidating and overwhelming experience. Here are some key questions to ask yourself and sellers before plopping down a down payment. Let me help you with my FREE homebuyer's class! Call me today! Laura Key 310.866.8422

Buying a house can be an intimidating and overwhelming experience. Here are some key questions to ask yourself and sellers before plopping down a down payment.

What To Ask When Looking At Potential Homes

Following is a list of general questions you should always ask when considering making a real estate purchase. Keep in mind, however, you are unique.

You have particular dislikes and likes as well as factors in your life that are different than other people. The point I am trying to make is that you shouldn’t stick to just these questions. You are making an important choice, so give some thought to your situation.

1. Don’t rush into things. The first question to ask should be directed at yourself. What type of home do you want? How big should it be? What amenities do you want? Are you planning for a family in the next three to five years and will the home be able to accommodate a new bundle of joy? Make a definitive list and stick to it. If you stray from it, you could end up with a house that doesn’t really fit you and suffer buyer’s remorse.

2. The next question is what area do you want to live in? Pick a few. You may find the prices to be excessive or the selection not so hot, but make sure you exhaust those areas before moving on. Again, you want to avoid buyer’s remorse.

3. Once you start looking at homes, a key question to ask is how long the house has been on the market. The amount of time will give you an idea of how flexible the owner is on price. If the house has been on the market for a month, the owner isn’t going to be very flexible. If it has been on the market for six months, flexibility will definitely exist.

4. Has the house previously been in escrow, but fell out? If so, find out why? Was it a problem with the buyer getting financing or did the buyer find out there was something wrong with the home?

5. What kind of condition is the house in and how old is it? Remember that a seller has typically done everything reasonably possible to spruce up the home. If you can see wear and tear on the house, it may be a red flag. In such a situation, you need to get a home inspection to make sure there aren’t problems in areas you can’t see such as mold, rust and water leaks.

6. If you have children or are planning on it, you must investigate the school district. Are the schools good? Are there gangs or crime in the area?

7. In addition to the home price, you should ask whether there are any additional fees such association fees.

8. What are the property taxes and what will they be when you buy? Many people are shocked to find out how much they have to kick out in property taxes. Don’t get surprised.

9. Zoning and easement issues are often overlooked when buying a home. If you are buying in a neighborhood with many homes, zoning is undoubtedly going to be for residential living. Easements, however, can be nasty surprises. Find out if there are any easements on the property. An easement gives a third party the right to use of part of the property. This can include giving the neighbor the right to do something or a utility company to place structures on your prospective property.

10. Noise is another big issue to consider. If you are serious about the property, make sure to drive buy on weekdays and weekends. If the property shares a wall with another residence, such as a duplex or condo, make sure you view it while the neighbors are home to get an idea of how loud it is.

11. In the euphoria of buying a property, practical issues can be missed. A big one is traffic. Specifically, what is the commute like between the house and your place of work? You don’t want to buy the house only to find out it takes three hours to get to and from work each day.

Obviously, you should be asking many additional questions before making a purchase. These 11 questions, however, will help you get started. Call me to schedule a time to discuss the homebuying process in more detail. Don’t forget to look into fun things to do in the area to make sure it’s where you want to live!I care about my clients and educating them is a priority! Laura Key 310.866.8422 or email me at Laura.A.Key@gmail.com

What to Expect At a Foreclosure Auction

Whether you are an investor that would like to get into buying foreclosed homes for your personal use! Call me today! Laura Key 310.866.8422

Whether you are an investor that would like to get into buying foreclosed homes for your personal use or to flip the property or if you are having your home foreclosed on, you should know what to expect at a foreclosure auction. Of course, the actual steps that will be taken can vary a bit from state to state and from house to house, but it’s good to know what you will be getting into when you go to a foreclosure auction. Foreclosure auctions can be exciting, even fun, but knowing what to expect will help you make the most of the experience, whether you are an investor or a homeowner that is trying to get your house back.

Before the Auction

You’ll likely find out about the foreclosure auction in a local newspaper and on the flier may be information to pre-qualify for bidding. This will allow you to put down a deposit so that the auctioneer knows that you are a serious bidder and can fulfill your bid if you are the winning bidder. Being pre-qualified just sort of speeds up the process so that you don’t have to mess around with the deposit on the day of the auction. During this time you should also do some research on the house by looking into any liens that may be against the property, how much the property is worth, how much it has appreciated in the last few years, as well as property values in the area. If the home looks as though it will need some repairs, you should consider this as well when trying to come up with how much you will be willing to pay for the house. Without this research, no amount of knowledge about what goes on at a foreclosure option will help you because you won’t know where to start when it comes to actually making a good bid.

What Happens At the Auction

The auction will typically start with the auctioneer reading legal notices as well as a legal description of the property. The auctioneer will usually then begin taking bids on the property. If the auctioneer has pre-qualified bidders the process is more streamlined, if not, each time a bid is made the auctioneer will then ask for the bidders deposit check, which is typically right around $5,000 for residential auctions. After each bid the auctioneer will attempt to solicit bids for higher amounts. Each auction is different, but the auction increments usually are set by the auctioneer and may be by $100, $500, or $1,000 per bid. The auctioneer will continue to solicit bids by this increment until it is clear that the highest bid has been reached. Then, the auctioneer will announce, “Going once, going twice, three times, sold!” indicating that the auction is over and the property has been sold to the highest bidder.

Once the bidding has ended a foreclosure deed and purchase papers will be drawn up and validated by the new owner or purchaser and the mortgage holder. A grace will likely be given to allow the purchaser to find financing or to come up with the funds to cover the full amount of the bid. This grace period is usually 30 days unless the purchaser and the mortgage holder agree to other terms. After the grace period a closing will take place, so that the new owner can formally take the title to the property.

What Happens, Now?

The purchaser can do what he or she intended to do with the property, whether it is to move into the home or to sell it for full market value. The money paid by the purchaser will be distributed in order of priority, first of which would be taxes. After taxes money will be paid to the mortgage, then the second and third mortgage if applicable. If there is still money after paying these debts, remaining money will be paid to lien holders and creditors. There is a very slim chance that there will be money left over after all of the debts are paid, if this is the case then the monies will be paid to the former home owner.

What about the Original Owner?

The original owner will often be at the auction so that they can bid on their home, and this is legal as long as they have the deposit required. If the owner of the home that has been foreclosed does bid on the home they must remember that the deposit is not refundable and the deposit assumes that they will be able to finance the home within the grace period. Owners must also remember that if they buy the property back old debts may merge and become reinstated such as second and third mortgages that became void when the first mortgage foreclosed on the property unless one has filed bankruptcy and is truly free and clear of these debts. Owners will often drum up the funds to make the deposit so that they can have another 30 days to try to save their home. Owners may or may not be successful in their attempts to save their home at a foreclosure auction.

As you can see, there are a lot of things that go into a foreclosure auction, but none of them are all that difficult to understand, but knowing about them makes the auction more enjoyable. The auction itself is not all that complicated, but it can be very fast paced. At some foreclosure auctions there are a lot of people, at others there are only a few because of the location or just the debts attached to the property, or even the state of the property. If you are serious about the property you should pay close attention when bidding starts so that you are sure that you can get your bid in when you feel it’s time so that you have the best chance of being the top bidder.

Call me for more info! Laura Key 310.866.8422

3 Ways Renters Lose Money

Are you still renting a home or apartment for yourself or your family? If so, you're losing money. Besides losing out on making money with real estate, renters don't get the same satisfaction of home enjoyment that benefits home buyers. If you're renting, call me today to find out how to to buy your own home. Call me today! Laura Key 310.866.8422

Are you still renting a home or apartment for yourself or your family?

If so, you're losing money. Think about these three ways you lose money by renting:

1. You're paying for someone else's mortgage payment. You're missing out on the appreciation that the property gives to the landlord. Appreciation is a term used in accounting relating to the increase in value of an asset, which means in real estate terms, added value to the property. Over the past five years, houses appreciated significantly, making many new real estate investor multimillionaires.

2. Renters don't get to freeze their monthly housing expenses like home buyers can. Of course, many home buyers get mortgage payments with adjustable interest rates and their payments go up over time. However, these payments will not go up over the long term like rising rents. Just think about how much an apartment costs today compared to ten years ago. A two bedroom apartment in Lake Elsinore, California leases for $1,000 today. The exact same apartment rented for $325 in 1996, when it was brand new. Home buyers who had low monthly payments in 1996, who did not refinance their mortgage, enjoy low payments and don't have to worry about rising rents.

3. Renters don't benefit from tax advantages. Home owners get income tax deductions. Tax deductions for interest costs, for instance, save tax payers thousands of dollars.

Emotional Satisfaction of Home Ownership

Besides losing out on making money with real estate, renters don't get the same satisfaction of home enjoyment that benefits home buyers. Many landlords won't allow you to paint your walls in colors that you desire. Also, you won't feel like fixing up the property with custom window coverings and you get little say in flooring materials. Because you can't make your personal statement, you won't feel like you're HOME as much as home owners who feel emotionally connected to their property.

How to Buy Your First Home

The biggest barrier to home ownership is often accumulating funds for a down payment. People think they have to have thousands of dollars for a down payment. However, if you have good credit and a decent job, you can get a mortgage for a home with zero down. And you can finance some of your closing costs as well as ask the seller to help you pay a good portion of your purchase costs. With today's mortgage finance plans, you may be surprised to find out how much of a home you can afford with payments similar to what you currently pay in rent.

You may have to go out of the major metropolitan areas to buy a home. That's why so many people commute in Southern California. Affordable housing costs much less in outlying areas. But so do the rents. If you're renting an apartment for $2,300 in Los Angeles, you could buy a $500,000 home in Wildomar. Our daughter just purchased a home in December 2005 and her mortgage payment, for a 3,000 square foot new home, costs less than $2,300. With her tax savings, she will pay even less than renting a small apartment closer to downtown L A.

If these amounts sound high to you, check your local area. Perhaps your monthly rent is only $1,000 and houses cost less than $200,000. Talk to a mortgage loan officer and see how much of a home you can afford.

If you're renting, make one of your priorities to buy your own home.

Copyright © 2006 Jeanette J. Fisher

Definition of Prescriptive Easement

Call me if you have some questions about a Prescriptive Easement! I have a team that can help you if you have concerns! Laura Key 310.866.8422

A prescriptive easement creates a right to use another's land for a specific purpose. The easement is created by making use of the land without owner permission for a period of time specified by statute. Interference with a prescriptive easement gives the easement holder cause to bring suit.

Easement in General An easement creates a right to use land that is possessed by another for a specific purpose. One parcel of land, the "dominant tenement," enjoys the benefit of the easement, while the "servient tenement" is the land being used for the easement purpose. Once an easement is validly created, even if not used, it is presumed to be perpetual.

Prescriptive Easement A prescriptive easement is acquired when the servient tenement is used for a specific purpose, for some time without the permission of the owner. Through the continuous use and the owner's failure to stop it, the dominant tenement can acquire the right to use the servient tenement property indefinitely. A prescriptive easement is a type of easement appurtenant, meaning that the holder receives physical use or enjoyment of the property. All who may succeed to title of the dominant tenement will be entitled to the prescriptive easement; the easement need not be mentioned in the conveyance or deed in order to be operative.

Elements Speaking generally, for legal elements are usually required: adverse use (use of the servient property without permission of the owner); open and notorious use (with no attempt at concealment); continuous use for the entire statutory period (required statutory periods vary among states, but the minimum is five years); and hostility, meaning that hte easement user knowes he has no right to use the property. However, individual state' easement laws may display variations, and those with easement issues should consult a legal professional.

Exclusive Use Jurisdictions are split on weather a prescriptive easement requires that adverse use of the property be exclusive in order to fulfill the legal element. A minority of jurisdictions will not allow a prescriptive easement if other parties besides the dominant tenement have also been using the servient tenement adversely for the same use. However, most do not require exclusive use, only that the dominant tenement's right to adversely use the easement "does not depend on a like right in others". In other words, the dominant tenement may still get the prescriptive easement even if the owner or others are also using the tenement in a similar manner.

Termination of Easement As an owner may prevent establishment of a prescriptive easement by effectively ending the dominant tenements adverse use; this can be accomplished by bring suit or physically ejecting the easement user from the property. Easements can also be terminated in several ways; the easement holder can release the servient tenement from the easement; the dominant and servient tenement can merge ownership; or the servient tenement can be condemned. The servient tenement may also invalidate the easement by a sort of "reverse prescription," if the servient tenement uses the easement for a long time and the easement holder "sleeps on his rights."

Source: http://www.ehow.com/about_6501555_definition-prescriptive-easement.html

First comes home, then comes marriage?

Couples today are significantly more likely to purchase a home before marrying than older couples were, according to a survey commissioned by real estate franchisor Coldwell Banker that appears to point to a cultural shift in views toward homeownership and marriage.

Twenty-five percent of married couples between the ages of 18 and 35 bought their first home before their wedding date, compared to 14 percent of married couples who are 45 or older, according to the survey, which was administered by Harris Interactive on behalf of Coldwell Banker.

"While life goals and expectations continue to weigh on young couples, their views of homeownership are transcending their plans of marriage and starting a family, creating a direct effect on the patterns of buying a home altogether," said Dr. Robi Ludwig, Coldwell Banker's lifestyle correspondent. "What we're seeing is that young couples are switching up the order and purchasing their first home regardless of whether or not they have set a wedding date. This is a huge movement within the American culture. While younger generations may be focusing more on their career, and in turn waiting longer to get married and have children, they are not delaying their dream of homeownership."

Other findings of the study include:

- Eighty percent of homeowners surveyed said buying a home strengthened their relationship more than any other purchase.

- Thirty-five percent of married homeowners purchased their first home by their second anniversary.

- Ninety-three percent of homeowners who purchased their first home while married always planned on buying a home after marrying.

- Thirty-five percent of married homeowners wish they had bought a home earlier than they did.

Is your big day coming up! Time to settle into a nest! Call me today! Laura Key 310.866.8422

BY INMAN NEWS, MONDAY, APRIL 22, 2013. Inman News®

Does HUD Offer Financing On Their Homes?

Buying a HUD Home is not as difficult as you may think! I have helped many people purchase their 1st Home from HUD! Call me today for more details about the process! Laura.A.Key@gmail.com or Visit my website to sign up for FREE HUD Listings! http://www.KeyCaliforniaHomes.com

HUD does not provide direct financing to buyers of HUD Homes. Buyers must obtain financing through either their own cash reserves or a mortgage lender. If you have the necessary available cash or can qualify for a loan (subject to certain restrictions) you may buy a HUD Home. While HUD does not provide direct financing for the purchase of a HUD Home, it may be possible for you to qualify for an FHA-insured mortgage to finance the purchase.

Los Angeles HUD homes, Buying A Hud Home, North Hollywood HUD homes, Westchester HUD Homes, Gardena HUD Homes, Northridge HUD Homes, Santa Clarita HUD Homes, Simi Valley HUD homes, Lemert HUD Homes, Compton HUD Homes, Lynwood HUD Homes, Hawthorne HUD Homes, Inglewood HUD Homes, Baldwin Hills HUD Homes, Playa del rey HUD homes, Marina del Rey HUD Homes, Santa Monica HUD homes, Lakewood HUD homes, Buying A HUD Home, Buying a Los Angeles HUD Home, HUD Trained Agent, HUD NAID agent

HUD-Owned Homes Expected to Surge

Soon the market will be filled with new listings from HUD! Are you prepared? Make sure you use an agent who is HUD experienced and can help you find the home of your dreams. I have closed many HUD homes in the past few years! Let me assist you! Laura Key 310.866.8422

![]()

The U.S. Department of Housing and Urban Development is reportedly going to be releasing more of its homes to the market, which could be welcome news to buyers who have faced slim pickings in for-sale inventories.

Over the next two years, experts predict that HUD homes on the market will increase significantly as lenders work through the backlogs of foreclosures and foreclosure reviews.

“The inventory is there, [it’s] just not being released during the banks/servicers review of the loan/mortgage documents,” says Nat Genis, a HUD listing broker in Riverside County, Calif., which is already seeing an increase in HUD-owned homes.

"HUD homes are back," Genis told HousingWire. "FHA financing went away with the 'creative' financing of the 80/20 loans, and now with the increase of FHA financing, these government-backed loans guarantee that if the borrower defaults, HUD will pay off the mortgage, obtain the deed, and re-sell the home."

HUD-owned homes can be appealing because of the discounted sales price, even though they can be in poor condition often times, HousingWire reports.

HUD had 39,442 homes in its REO inventory nationwide as of Feb. 28, 2013—with 20,536 of those having pending contracts on them, according to HUD.

Source: “HUD homes add to inventory-starved market,” HousingWire (April 29, 2013)

Do I Need An Appraisal On A HUD Home?

Buying a HUD Home is not as difficult as you may think! I have helped many people purchase their 1st Home from HUD! Call me today for more details about the process! Laura.A.Key@gmail.com or Visit my website to sign up for FREE HUD Listings! http://www.KeyCaliforniaHomes.com

It is not necessary to have a HUD home independently appraised, HUD offers an appraisal every 6 months. Your Lender may require a more current appraisal than the one provided by HUD. Ask your loan officer or HUD registered agent.

Los Angeles HUD homes, Buying A Hud Home, North Hollywood HUD homes, Westchester HUD Homes, Gardena HUD Homes, Northridge HUD Homes, Santa Clarita HUD Homes, Simi Valley HUD homes, Lemert HUD Homes, Compton HUD Homes, Lynwood HUD Homes, Hawthorne HUD Homes, Inglewood HUD Homes, Baldwin Hills HUD Homes, Playa del rey HUD homes, Marina del Rey HUD Homes, Santa Monica HUD homes, Lakewood HUD homes, Buying A HUD Home, Buying a Los Angeles HUD Home, HUD Trained Agent, HUD NAID agent

How Much Money Will I Have to Put Down on a HUD Home?

Buying a HUD Home is not as difficult as you may think! I have helped many people purchase their 1st Home from HUD! Call me today for more details about the process! Laura.A.Key@gmail.com or Visit my website to sign up for FREE HUD Listings! http://www.KeyCaliforniaHomes.com

If the bid price is less than $50,000, you’re required to make an earnest money deposit of $500. HUD homes priced greater than $50,000 require a $1000 deposit.

Los Angeles HUD homes, Buying A Hud Home, North Hollywood HUD homes, Westchester HUD Homes, Gardena HUD Homes, Northridge HUD Homes, Santa Clarita HUD Homes, Simi Valley HUD homes, Lemert HUD Homes, Compton HUD Homes, Lynwood HUD Homes, Hawthorne HUD Homes, Inglewood HUD Homes, Baldwin Hills HUD Homes, Playa del rey HUD homes, Marina del Rey HUD Homes, Santa Monica HUD homes, Lakewood HUD homes, Buying A HUD Home, Buying a Los Angeles HUD Home, HUD Trained Agent, HUD NAID agent

Can You Buy a Home That Isn’t for Sale?

With inventory so low in Cali you must think outside the box. I'm willing to go there with you! Laura.A.Key@gmail.com

It may seem like an odd question, but apparently, you can!

This article is brought to you exclusively by RealtyPin.com

Should I Get A Home Inspection If I Am Buying A HUD?

Buying a HUD Home is not as difficult as you may think! I have helped many people purchase their 1st Home from HUD! Call me today for more details about the process! Laura.A.Key@gmail.com or Visit my website to sign up for FREE HUD Listings! http://www.KeyCaliforniaHomes.com

HUD does not warrant the condition of its properties and will not pay for the correction of defects or repairs. Since the new owner will be responsible for making needed repairs, HUD strongly urges every potential homebuyer to get a professional inspection prior to submitting an offer to purchase.

If you are interested in acquiring a HUD Home that is in need of repair, you may be interested in applying for an FHA 203(k) Rehabilitation Loan. When a homebuyer wants to purchase a house in need of repair or modernization, the homebuyer usually has to obtain financing first to purchase the dwelling; additional financing to do the rehabilitation construction; and a permanent mortgage when the work is completed to pay off the interim loans with a permanent mortgage. Often the interim financing (the acquisition and construction loans) involves relatively high interest rates and short amortization periods. The Section 203(k) program was designed to address this situation. The borrower can get just one mortgage loan, at a long-term fixed (or adjustable) rate, to finance both the acquisition and the rehabilitation of the property.

Will HUD make the repairs?

HUD homes are sold as-is. The new owner is responsible for all repairs and improvements.

Can I start improving on the property right away?

If HUD accepts your offer, you cannot make any repairs or home improvements until the escrow transaction has closed and title is recorded in your name.

Los Angeles HUD homes, Buying A Hud Home, North Hollywood HUD homes, Westchester HUD Homes, Gardena HUD Homes, Northridge HUD Homes, Santa Clarita HUD Homes, Simi Valley HUD homes, Lemert HUD Homes, Compton HUD Homes, Lynwood HUD Homes, Hawthorne HUD Homes, Inglewood HUD Homes, Baldwin Hills HUD Homes, Playa del rey HUD homes, Marina del Rey HUD Homes, Santa Monica HUD homes, Lakewood HUD homes, Buying A HUD Home, Buying a Los Angeles HUD Home, HUD Trained Agent, HUD NAID agent

Is There Anyway To Have My HUD Offer Considered Before Others?

Buying a HUD Home is not as difficult as you may think! I have helped many people purchase their 1st Home from HUD! Call me today for more details about the process! Laura.A.Key@gmail.com or Visit my website to sign up for FREE HUD Listings! http://www.KeyCaliforniaHomes.com

Owner occupants always have first priority; however, if there are not any bids after the 30th day then bidding is open to all bidders (investors). All offers are due by the bidding date and the HUD system generally picks the highest and best offer.

Los Angeles HUD homes, Buying A Hud Home, North Hollywood HUD homes, Westchester HUD Homes, Gardena HUD Homes, Northridge HUD Homes, Santa Clarita HUD Homes, Simi Valley HUD homes, Lemert HUD Homes, Compton HUD Homes, Lynwood HUD Homes, Hawthorne HUD Homes, Inglewood HUD Homes, Baldwin Hills HUD Homes, Playa del rey HUD homes, Marina del Rey HUD Homes, Santa Monica HUD homes, Lakewood HUD homes, Buying A HUD Home, Buying a Los Angeles HUD Home, HUD Trained Agent, HUD NAID agent

Rising Student Loan Debt Keeps Buyers Out

There are simple solutions around this issue. Call me today to discuss your options! Laura Key 310.866.8422

Between 2004 and 2012, student loan balances nearly tripled, according to a new survey from the Federal Reserve Bank of New York. What’s more, one-third of student loan borrowers are delinquent on their debt, according to the Federal Reserve report. This will impact their credit rating and possibly keep them out of the mortgage market much longer.

"Short term, you see a decrease in the number of first-time home buyers," Brian Coester of Coester Valuation Management told CNBC. "You're going to see somebody who would have been able to afford a more expensive house maybe go for the lower version or the downgraded version."

Potential buyers with heavy student debt burden have been forced to rent or even move back in with their parents as they chip away at their debt.

"Long term it's going to really affect especially the upper end, because people aren't going to have the excess income to buy the jumbo property or buy that high end property," says Coester. "It' s going to affect home prices as a negative, as more of a cap, because it's really debt that they are servicing."

Source: “Student Debt Is Housing’s $1 Trillion Challenge,” CNBC.com (April 8, 2013)

Economist Quashes Housing Bubble Rumors

I love what I do; however I have reservations about this report. I have had deep conversations with other agents and I firmly feel we are in a danger zone. Your thoughts? Laura Key 310.866.8422

Recently, rumblings of another housing bubble have been emerging, but one economist says with inventories expected to rise soon, the housing market is not at threat.

Rick Sharga, executive vice president with Carrington Mortgage Holdings, told a crowd at the REOMAC 2013 Summit & Expo in Dallas on Monday that the housing market should expect things to get worse before they start improving.

But “this is not the 2005 market,” he said. “We are not creating a bubble.”

Sharga says the lack of available home inventory is the reason why home prices are rising. New-home inventories are at their lowest level in more than 30 years, he said. “Very few markets are anywhere near where we were at the peak,” he said. The markets showing some “bubble-like tendencies” are housing markets that saw the biggest declines, he noted.

LPS Applied Analytics recently predicted that home prices could rise another 35 percent without affecting affordability.

Sharga predicts that by this time next year there will be too many homes for sale. Housing and foreclosure starts are expected to start rising within the next year.

Source: “Carrington’s Sharga: We Are Not Creating Another Housing Bubble,” HousingWire (April 8, 2013)

When Can I Bid on a HUD Home?

Buying a HUD Home is not as difficult as you may think! I have helped many people purchase their 1st Home from HUD! Call me today for more details about the process! Laura.A.Key@gmail.com or Visit my website to sign up for FREE HUD Listings! http://www.KeyCaliforniaHomes.com

Owner occupants can offer a bid on a HUD home during the first nine days. HUD will look at all bids on the 10th day and decide based on which offer gives them the highest net profit. If there are two or more bids at the same net to HUD the offers will go into a lottery and the bid will be awarded based on chance. After the 10th day if there aren’t any acceptable bids there will be an additional 20 days of bidding where bids are opened and reviewed daily for owner

Los Angeles HUD homes, Buying A Hud Home, North Hollywood HUD homes, Westchester HUD Homes, Gardena HUD Homes, Northridge HUD Homes, Santa Clarita HUD Homes, Simi Valley HUD homes, Lemert HUD Homes, Compton HUD Homes, Lynwood HUD Homes, Hawthorne HUD Homes, Inglewood HUD Homes, Baldwin Hills HUD Homes, Playa del rey HUD homes, Marina del Rey HUD Homes, Santa Monica HUD homes

Does Moving Up Make Sense?

Don't get caught up in the madness of the market. Deciding to sell is a personal decision, take everything into account. I am here to assist! Laura Key 310.866.8422

These questions will help you decide whether you’re ready for a home that’s larger or in a more desirable location. If you answer yes to most of the questions, it’s a sign that you may be ready to move.

- Have you built substantial equity in your current home? Look at your annual mortgage statement or call your lender to find out. Usually, you don’t build up much equity in the first few years of your mortgage, as monthly payments are mostly interest, but if you’ve owned your home for five or more years, you may have significant, unrealized gains.

- Has your income or financial situation improved? If you’re making more money, you may be able to afford higher mortgage payments and cover the costs of moving.

- Have you outgrown your neighborhood? The neighborhood you pick for your first home might not be the same neighborhood you want to settle down in for good. For example, you may have realized that you’d like to be closer to your job or live in a better school district.

- Are there reasons why you can’t remodel or add on? Sometimes you can create a bigger home by adding a new room or building up. But if your property isn’t large enough, your municipality doesn’t allow it, or you’re simply not interested in remodeling, then moving to a bigger home may be your best option.

- Are you comfortable moving in the current housing market? If your market is hot, your home may sell quickly and for top dollar, but the home you buy also will be more expensive. If your market is slow, finding a buyer may take longer, but you’ll have more selection and better pricing as you seek your new home.

- Are interest rates attractive? A low rate not only helps you buy a larger home, but also makes it easier to find a buyer.