BLOG

Beautiful Tile Work

This beautiful tile work was found in a bathroom located by the pool! Just Gorgeous! Its bright and detailed. In my opinion you just can't go wrong with mermaids by a pool.

Buyers: Ready to find your new home? Sellers: Want to see what homes are being listed at in your neighborhood?

It's easy! Text LKHOMES to 87778 for free MLS application.

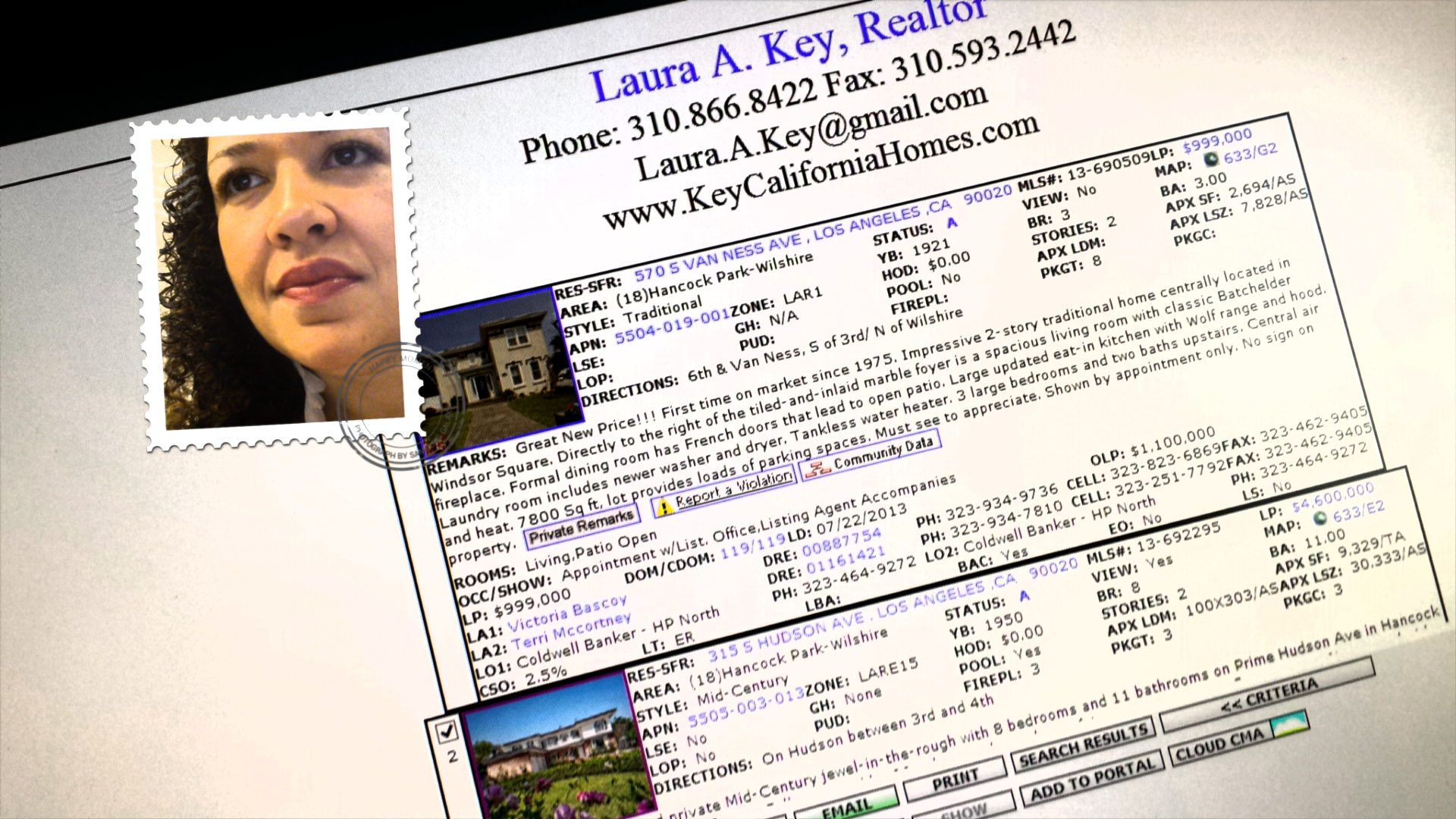

Hard at Work In Real Estate

Looking for A New Home? Text LKHOMES to 87778 to get instant free access to the MLS! Or Call me at 310.866.8422

Homes are turning over quickly in Los Angeles! Let me work hard for you!

California Real Estate, Los Angeles Homes, Homes for Sale, Larchmont Homes for Sale, Hancock Park Homes for Sale, Windsor Square Homes for Sale, West Hollywood Homes for Sale, Koreatown Homes for Sale, Realty Goddess, Top Los Angeles Real Estate Agent, Real Estate Agent, Realtor, MLS, Home Search

My New Favorite House in Hancock Park

Call Me for More Details 310.866.8422

Call Me for More Details 310.866.8422

I see a lot of homes daily, so when I came across this beautifully restored home located in Hancock Park my heart leap. For the past two years I have driven by this beauty on my way home, but one day I saw a fellow agent placing a "For Sale" sign outside beside the lovely rose garden! I rushed home to look up the details and saw it was going to be an open house. That Sunday my first agenda was to see this house and what I found made me fall in love more.

- 8 bedrooms 8 Bathrooms

- 12 foot ceilings

- 3 Floors

- Private nooks

- Garage with additional living/working space

- Rose Garden

- Porch

- Mature tree in the front yard

- Apx SF 6000 on a 9470 Lot

This home has history, it was been LOVINGLY restored to it's original glory and no detail was spared. This home is one that you simply must see and in my opinion is priced perfectly.

The time is perfect to purchase your new home! Text LKHOMES to 87778 to find your next home FREE! My app gives you DIRECT access to the SoCal MLS. No more fluff, no more outdated listings....just homes at your fingertips! Call me today! 310.866.8422

What Buyers Want and Are Willing to Pay For It!

Find homes from your phone for FREE! Text LKHOMES to 87778 and download the MLS application! No fluff, no signing up...just homes at your fingertips!

Beware of Rental Scams

Warning Regarding Online Rental Schemes

By Wayne S. Bell, Real Estate Commissioner California Bureau of Real Estate

Issued: October 2013

In prior consumer alerts, the California Department of Real Estate, the predecessor of the California Bureau of Real Estate (“CalBRE”) issued warnings to prospective renters about (i) imposter landlords and (ii) scams perpetrated by or in connection with Prepaid Rental Listing Services.

There are almost endless varieties of real estate and rental fraud. Some are new. Many are old, and some are just variations on timeworn scams.

CalBRE has received reports and been made aware of online rental scams (often using such Internet sites such as Zillow, Trulia, Craigslist, and HotPads), and we want to warn the public about some of the most common ones.

Included in this warning is a list of “red” flags or signs to look for, suggestions on how prospective renters can protect themselves, and reporting recommendations for those potential renters who have been victimized.

Common Scams

In most cases, the fraud involves a scammer who:

- Duplicates or “hijacks” an actual listing of a property that is for rent.

- Creates a fake or fictitious listing for a rental property.

- Offers for rent a real, but unavailable, property.

- Rents a property that is in foreclosure and which will soon be sold, or that has been fully foreclosed (or is in pre-foreclosure).

In the cases mentioned above, the perpetrators do not own the properties (although they oft-times pretend to be the owners) and they are not authorized or licensed to rent the properties.

In most of these cases, the scammers collect money (usually via wire transfer) from the victims for deposits, fees and rents, and in a number of the cases obtain enough personal information, such as social security, driver license and bank account numbers, to steal the identities of the “renter” victims.

For the fraudsters, these are crimes of opportunity and they are simply taking advantage of individuals who are looking for rental housing in a tight real estate market. The perpetrators engage in these crimes (via the Internet ether) because they have found success with such scams and continue to find victims who send money and/or who provide personally identifying information that can be used by the scammers to commit additional crimes.

Please see Consumer Alert – Beware of Imposter Landlords and Consumer Fraud Alert and Warning – Prepaid Listing Services (PRLS).

Because of the anonymity and widespread availability of the Internet, an online rental scam can be started and operated from anywhere in the United States or in other countries.

“Red” Flags

While none of the “red” flags below is definitive proof of fraud, the following are warning signs of a possible scam:

- The advertised rental rates are low (many times very low) compared to other rentals in the area. Always remember the time-tested adage that if something seems too good to be true, it probably is.

- The purported landlord or agent requests that the advance payment of rents and deposits (and possibly other fees) be made via cash or wire transfer (such as Western Union), and/or asks for personal information such as social security number, bank account information, and driver license number. It is important to note that payments made by cash or wire transfer provide little – and usually no – recourse, especially since the scammer to whom the funds are wired usually disappears and cannot be found. While credit card payments are not accepted by many landlords or property rental agents, prospective renters should – to provide an amount of self-protection – ask to pay for rents, deposits and fees by credit card.

- The supposed owner or rental agent is either out of the country or in another State, or is in a hurry to leave California, and states that the rental property cannot be shown or toured.

- The prospective landlord or property agent is not willing to meet in person, and/or applies pressure to complete the rental transaction as soon as possible.

Ways that Prospective Renters Can Protect Themselves

The best advice for prospective renters is to be wary, and to conduct their own diligence and investigate the person with whom they are dealing or negotiating, and the property itself. In this regard, potential renters should:

- Confirm or verify the identity of the supposed landlord or property agent. To see who owns the property, contact a licensed California real estate agent, the county recorder’s office in the county where the property is located, and/or a title company. Talk with neighbors about the property and ask who owns it, and ask a lot of questions about the rental history of the property. If dealing with a property manager or leasing agent (who does not live at the property), look them up on the CalBRE website (www.bre.ca.gov) to see if they are licensed. If they are, check to see if they are disciplined or otherwise restricted in the real estate practice that they can do. Also, check the person out on Google or other search engines, and through the Better Business Bureau.

- Confirm that the property is not in foreclosure or pre-foreclosure. This is especially true when renting a house. The mortgage loan should be in good standing and not in default.

- Not rent a property without viewing and touring it in person.

- Not pay or transfer any money without reviewing all rental documents, and getting copies of all writings pertaining to the property.

- Demand to meet and then actually meet the supposed owner or property manager in person, and ask many questions about the property and the neighborhood.

- Work with an experienced, competent, and licensed California real estate broker, or salesperson working under the supervision of a broker.

- Take photographs of the property.

- Not pay anything in cash or wire transfer money.

- Do research on what comparable properties rent for.

The essential point here is that prospective renters, in order to protect their interests, and not become a scammer’s next victim, must remain skeptical, proceed cautiously, do their own investigation of the property and individuals involved with the rental(s), and be aware of and look for revealing signs of fraud.

After Falling Victim or Becoming Aware of an Online Rental Scam

If a prospective renter has been scammed, or becomes aware of an online rental scam, he or she should immediately report the fraud and file complaints with one, more or all of the following:

- The relevant Internet provider (e.g., Zillow, Trulia, etc.).

- CalBRE if a real estate licensee is involved, or if the scammer is unlicensed and purporting to be a real estate agent. Please contact CalBRE at www.bre.ca.gov.

- The California Attorney General, at www.oag.ca.gov/consumers.

- The District Attorney, Sheriff, local police and local prosecutor in your community.

- The Federal Trade Commission, at www.ftc.gov.

- Federal Bureau of Investigation (FBI), at www.fbi.gov.

- The Consumer Financial Protection Bureau at www.cfpb.gov.

Issued: October 2013

Call Laura Key for your real estate needs, rentals, sales, purchase, investment! 310.866.8422 Search for homes NOW!

FHA Limits for Los Angeles Area

Homeownership is not out of reach. FHA limits in California are one of the highest in the country. I have great lenders that can help you reach your real estate goals! Call me to get started on your homeownership goals!!! Laura Key 310.866.8422

Here are the current limits for Los Angeles (as of August 23, 2013) FHA allows 3.5% downpayment over a 15 to 30 year term!

Single Family $729,750

Duplex $934,200

Tri-Plex $1,129,250

Four-Plex $1,403,400

Source: FHA.com

Feds Sue BofA over 2008 Bonds Backed by Prime Jumbo Mortgages

The federal government is accusing Bank of America Corp.of securities fraud, saying the second-largest U.S. lender lied to investors about flaws in supposedly prime loans, including some resembling subprime "liar loans," when it sold $850 million in mortgage bonds in 2008.

Lawsuits filed by the U.S. Justice Department and Securities and Exchange Commission are the latest in a long string of government and private mortgage-related civil actions targeting banks. BofA has drawn a disproportionate number because of the liability it shouldered in 2008 when it acquired the enormous subprime lender Countrywide Financial Corp. of Calabasas.

The new DOJ and SEC suits, filed Tuesday, are the first such government suits not to involve Countrywide, instead accusing BofA itself of wrongdoing. In another unusual twist, they focus on jumbo mortgages -- the outsized home loans designed for wealthy borrowers.

The SEC said losses so far to investors in the mortgage-backed securities have totaled about $70 million and may eventually reach as high as $120 million. The investors included the Federal Home Loan Bank of San Francisco andWachovia Bank, the East Coast giant that nearly failed and now is part of Wells Fargo & Co.

A BofA statement blamed the housing market collapse for defaults in the pool of loans backing the bonds, and said they performed better than similar bundled loans from that era. The bank maintained that it would show the bonds were bought by "sophisticated investors who had ample access to the underlying data" -- but presumably didn't bother investigating.

The DOJ said BofA made most of the loans through mortgage brokers, not telling the investors that it had learned at the time that these loans were defaulting at a high rate. BofA no longer makes mortgages through third-party channels.

Despite the affluent clientele, about 15% of the mortgages resembled the subprime "liar loans" that led to so many defaults, the DOJ suit said. These "Paper Saver" loans were made to self-employed borrowers without bank verification of their income or assets, it said, accusing BofA of not disclosing the percentage of the loans made in this high-risk manner.

"As Defendants knew, mortgages given to self-employed borrowers were more risky than mortgages given to salaried borrowers and stated income/stated assets mortgages given to self-employed borrowers were even riskier," the lawsuit said.

The DOJ lawsuit alleged violations of a 1989 law that allows the government to seek hefty civil penalties. It says that in addition to other problems, BofA violated its own underwriting standards in issuing the loans and did not perform a due-diligence investigation at the loan level when it securitized them.

Source: LATimes By E. Scott Reckard August 6, 2013, 4:45 p.m.

More Renters Say They Want to Own, Survey Finds

Interested in purchasing a new home! I have a team that can help you reach your real estate goals! Call me today! Laura Key 310.866.8422

The majority of renters say home ownership is one of their highest priorities for their future, and more renters are saying they want to buy soon, according to the 2013 National Housing Pulse Survey, conducted by the National Association of REALTORS®. Renters are showing stronger desires for home ownership compared to recent years, according to the survey.

“Home ownership matters to Americans who consistently realize the many benefits it provides to communities, families, and the nation’s economy,” says NAR President Gary Thomas. “Due to high housing affordability and today’s interest rates it makes sense for people to consider home ownership over renting. In fact, in many parts of the country it’s cheaper to own a home than to rent one. Therefore, it’s no surprise that renters recognize that owning a home offers tremendous long-term benefits and is an investment in their future.”

Fifty one percent of renters say that eventually owning a home is one of their highest personal priorities, up from 42 percent in the 2011 survey.

The survey found that 80 percent of the 2,000 Americans surveyed say they believe buying a home is a good financial decision. Sixty-eight percent said now is a good time to buy a home, too.

Their main motivations to home ownership: Building equity, wanting a stable and safe environment, and the freedom to choose where to live, the survey found.

Meanwhile, the main obstacles to home ownership have remained the same over the years: saving for the down payment, closing costs, low wages, and student loan debt.

“Student loan debt is a concern for many consumers in today’s market, especially first-time buyers,” Thomas says. “Buyers with student loan debt may find it difficult to access mortgage credit, as well as save for a down payment. Pending mortgage finance regulations requiring higher down payments could also contribute to the already tight lending environment. REALTORS® are working with regulators to address this issue and are committed to making sure those who are willing and able to own a home have the opportunity to pursue that dream.”

IRS Simplifies Home Office Deduction

Working from home can be beneficial! Hope these tips help! Need a home checkup? Call me Laura Key 310.866.8422

The number of home owners who work from home at least one day a week increased nearly 10 percent — from 9.5 million to 13.4 million — between 1999 and 2010, according to U.S. Census Bureau data. However, only 3.4 million home owners claimed deductions for business use of a home in 2010, according to the IRS.

The IRS recently announced a new safe harbor provision for home office deductions for the 2013 tax year.

“This allows at-home workers the option to simply take a deduction capped at $1,500 per year based on $5 a square foot for up to 300 square feet,” FOX Business reported. “The requirement that home office space be exclusively used for business and limitations on income earned from that business still applies, and direct business expenses unrelated to the home (advertising, supplies and wages paid to employees, etc.) are fully deductible.”

"The home office deduction is one of the most misunderstood and abused deductions out there," says Margaret Munro, a tax consultant, about the changes. "If you have a valid home office, you take the deduction because you shouldn't be paying tax on money that you're using for your business."

For more information on the deduction, visit the IRS Web site.

Source: “IRS' Simpler Home Tax Deduction Cuts Through the Clutter,” FOX Business (July 24, 2013)

Sellers Jack Up Price After Offer is Accepted

Until a contract is SIGNED it is not accepted! Be very careful when "words" or a simple "handshake" is used! It might come back to haunt you! Laura Key 310.866.8422

Some home sellers are accepting a buyer’s offer, even having a contract drawn up, only to ask for a higher price a few days later.

The move called “goalpost-shifting” is becoming more common in competitive markets with limited inventories of homes for sale, The New York Times reports. Some sellers keep the bidding on their homes going even after they’ve said they'll accept an offer from a buyer.

The New York Times describes a recent incident where a buyer offered $912,000 for a condo that was originally listed for $800,000, which had attracted more than a dozen offers. The seller accepted the buyer’s offer and a contract was written. However, a few days later the seller notified the buyer that the price had increased to $995,000. The buyer refused to increase his offer, and lost out on the unit. The seller ended up selling to another buyer who offered $1.1 million.

The practice is controversial, but The New York Times quotes brokers who note that buyers are learning a tough lesson: Until signatures are on a contract, a deal isn’t done. Also, they note the buyer is generally given the opportunity to increase their offer. However, other agents say it’s a greedy move on sellers’ part and that once sellers give their word, they should honor it.

“It’s surprising how ugly it’s getting,” says Robert Frankel, a real estate lawyer who frequently handles closings. “If you don’t hear back about a contract in two days, there are usually some shenanigans going on.”

Source: DAILY REAL ESTATE NEWS | MONDAY, JULY 22, 2013

The Real Estate World is moving and shaking, make sure you have an expert to help you during these times. Call Laura today! 310.866.8422

New House - New Yard - Got Plans?

What would you do with your new yard? Call me and let's get you started! Laura Key 310.866.8422

Condominiums – Should You Consider Purchasing One

Condominiums tend fall into the love them or hate them position for buyers

Condominiums are all about communal living, which can be good or bad depending upon your personal views. This type of communal living doesn’t refer to the failed experiments of the sixties wherein hippies packed into a structure and shared everything. Instead, the modern condominium community is all about sharing common spaces as well as rules, rules and more rules.

Condominiums come in all shapes and forms. Condos can be found in a single high rise building in a downtown area or in an apartment complex type of layout in a planned community. The structure isn’t the determining point. Instead, the issue is how the properties are owned.

Unlike a stand alone home, the property lines on a condominium are the walls of the structure. Essentially, you own everything inside the condominium as your individual property. Everything outside the condominium is owned jointly with the people who own the other units. These areas are known as common areas and are subject to group rule.

Every condominium has a homeowners association in one form or another. The association has rules set out by the original developer regarding landscaping and so on. Members of the community are then elected to the board of the association, whereupon the immediately become a focal point of aggravation from individual owners and often wonder why they took the thankless job.

The problem with the association and condos in general is the issue of uniformity. If you desire to change the exterior of your condominium in some way, you must comply with the rules of the association. This means you cannot paint your property a different color, do landscaping and so on. For some people, this isn’t a problem, but others are frustrated they can’t express themselves.

When deciding whether a condominium is a good option for your next purchase, you need to carefully weigh the restrictions of a particular association. If you consider yourself an individual and want to show it, a condominium is probably a very poor choice for you.

Clean Home, Easy Sale

One of the biggest problems people run into when selling their home is the process of preparing it for sale. The best way to begin this process is to take a quick walk through your home then call me for an appointment! Laura Key 310.866.8422

One of the biggest problems people run into when selling their home is the process of preparing it for sale. Many homes are simply places where we keep the accumulated treasures of the years. Are you a clutter-bug, a pack-rat? It's OK, we all are to some degree. When preparing a home for sale, we need to be mindful of our "stuff." The best way to begin this process is to take a quick walk through your home. Make a list of everything that you have not used in the past 3 months, 6 months? Now, and here is the hard part. Get rid of it. Seem a bit extreme? It might, but things that you have not used in half a year are not likely to get used in the future. Remember we are trying to get rid of some stuff so that people can see the house, not what's in it.

There is a common line of thought that home buyers want to see the "personality" of the homes current owners. This is not true. Buyers want to be able to see their belongings in the home. They want to put their personality into it to see if they could see themselves living there. A backlog of your stuff will get in the way of them doing this. Go through every room in turn and remove the clutter! This includes the closets, shelves and cupboards. Also remove excess furniture if the room seems too crowded. Here is another important thing to remember, don't put all this stuff in the garage! Buyers will go through the garage like any other room in your home. Hire a storage locker if it is really necessary. Aside from that, use this as an opportunity to rid yourself of those things that you never use.

The minimalist approach is a good thing to utilize when showing your home. The lack of personal effects will make it easier for buyers to place themselves in your home. This will also make the moving process easier on you. With less things to pack when moving day comes, you can dedicate more time to creating your perfect space in your new home.

Laura Key, BRE 01908085 310.866.8422 Laura.A.Key@gmail.com www.KeyCaliforniaHomes.com

Budget for Closing Costs – Home Inspection and Title Fees

Buying a home means you also have to budget for additional expenses! Make sure you put some money aside for the extras.

Purchasing a home is a euphoric event. Once escrow begins, the euphoria can change to frustration, particularly if you are not ready for the closing costs that quickly accumulate.

Closing costs simply refer to the fees associated with various things associated with the escrow process in a real estate transaction. In the excitement of having an offer accepted for your dream home, you can easily lose track of the fact you are going to need to have some serious cash on hand to pay them. Many people make the mistake of only assuming they need the down payment money, and have to rush around town trying to come up with money for the closing fees.

If you are buying a home, you need to get a professional home inspection. Doing so can reveal potential problems with the home that you wouldn’t otherwise notice. Problems can include things such as rot, termites, water leaks and a bevy of other issues. The time to do this is during escrow. Of course, that means you are also going to have to pay for the inspection. Depending on the size of the property, home inspections can run a few hundred dollars up to a few thousand. Make sure you have money set aside for the fees.

Title insurance is something you absolutely must purchase when you buy any real property, a home, building, land or whatever. Title insurance protects both you and your lender. Title insurance is just what it sounds like. A title company will research the title of the home and essentially guarantee that the title is good. This means the seller actually owns the title and has the right to sell it to you. The title company will also make sure there aren’t any liens on the homes or other things that will cause you problems. Depending on the price of the home, title insurance can run you a couple of hundred dollars or up into the thousands. Again, it is important to find out the cost and budget for it.

Title insurance and a home inspection are two things you should absolutely have when purchasing a home. Just make sure you budget for them.

Laura Key, BRE 01908085 310.866.8422 Laura.A.Key@gmail.com www.KeyCaliforniaHomes.comA Bit About Mold

There are a number of little things to look out for when purchasing a new home. Normally the things to consider includes such things as location, wiring, the condition of the house itself, and several other factors. One of these factors that the home buying public is becoming more concerned with is mold.

There are a number of little things to look out for when purchasing a new home. Normally the things to consider includes such things as location, wiring, the condition of the house itself, and several other factors. One of these factors that the home buying public is becoming more concerned with is mold. There are many different types of mold that can occur in a home and lead not only to structural damage, but some health concerns as well. Mold is difficult to find in many homes as it grows exclusively in dark and moist areas that are usually hidden somewhere in the structural areas of the home such as attics and basements. By the time mold shows up in the actual living areas, chances are that it is all through the home.

There are a number of little things to look out for when purchasing a new home. Normally the things to consider includes such things as location, wiring, the condition of the house itself, and several other factors. One of these factors that the home buying public is becoming more concerned with is mold. There are many different types of mold that can occur in a home and lead not only to structural damage, but some health concerns as well. Mold is difficult to find in many homes as it grows exclusively in dark and moist areas that are usually hidden somewhere in the structural areas of the home such as attics and basements. By the time mold shows up in the actual living areas, chances are that it is all through the home.

One of the most likely places for mold to form is anywhere that moisture is improperly vented. Another area of concern is if a home has ever flooded and was not completely or properly cleaned and dried after. Leaky plumbing and basement crawlspaces are other likely candidates. Mold can be a difficult thing to completely get rid of as the only thing it needs to continue growth is an organic material such as wood, and moisture. Both of these items are usually abundant in any home. The most likely was that moisture finds its way into the home is through faulty or leaky roofs and foundations. Both of these areas should be checked over by an experienced mold inspector on a fairly regular basis if there is any worry of mold beginning to grow, or if these has been mold in the past. Mold can be an expensive problem to deal with so be pro-active about looking for it, it can save you money in the long run.

Search for Homes Free! Click below!

Bank Faces Lawsuit Over Excessive Fees

Are you facing or someone you know facing foreclosure? There are sources out there to help you! Call me for a list of free resources! Laura Key 310.866.8422

JPMorgan Chase faces a lawsuit that alleges the bank imposed overly high or unnecessary fees on delinquent borrowers. The banking giant tried to get the case dismissed, arguing to the courts that the claims were unjust, but a federal judge ruled the lawsuit should proceed.

Borrowers are accusing the bank of “imposing excessive or unnecessary fees to inflate profit, including on services performed by third party vendors, cheating thousands of already-strained borrowers out of millions of dollars,” Reuters reports.

Among the fees in question range from $95 to $125 for “broker’s price opinions.” The plaintiffs, who reside in Tennessee, California, and Oregon, claim that the BPOs cost $30 to produce and that according to Fannie Mae guidelines they should not cost more than $80.

Similar lawsuits over mortgage fees charged to delinquent borrowers are pending against Wells Fargo and Citigroup.

Source: “JPMorgan must face lawsuit challenging mortgage fees,” Reuters (June 14, 2013)

Where Asking Prices Are Rising the Most

California is rising fast, yet it's not at the highest it's ever been. Interested in buying or selling! Let me assist you in reaching your real estate goals! Laura Key 310.866.8422

Median list prices in May edged up 2.10 percent month-over-month, as housing inventories also were on the rise, creating a greater balance between supply and demand, according to realtor.com’s latest Real Estate Health Report.

The nationwide median list price was $199,000 for May, and up 4.79 percent year-over-year.

"We are seeing large regional markets across the country leading the way to national recovery. These regions are acting as a microcosm for what's slowly happening in the larger real estate market," says Steve Berkowitz, chief executive officer of Move. "Overall, we're seeing seller confidence beginning to respond to consumer demand. Nationally, there are more homes going on the market for a shorter amount of time. And this is happening in our hot markets on a much larger scale."

California housing markets are seeing some of the highest median price gains. The following 10 markets have seen the highest year-over-year list price gains:

1. Sacramento, Calif.: up 42.45%

- Median list price: $284,900

2. Oakland, Calif.: up 38.27%

- Median list price: $495,000

3. Detroit, Mich.: up 31.73%

- Median list price: $125,000

4. San Jose, Calif.: up 30.58%

- Median list price: $679,000

5. Los Angeles-Long Beach, Calif.: up 27.80%

- Median list price: $428,000

6. Fresno, Calif.: up 27.48%

- Median list price: $219,900

7. Phoenix-Mesa, Ariz.: up 27.03%

- Median list price: $235,000

8. Stockton-Lodi, Calif.: up 25.63%

- Median list price: $199,750

9. Reno, Nev.: up 24.23%

- Median list price: $235,900

10. Santa Barbara-Santa Maria-Lompoc, Calif.: up 24%

- Median list price: $775,000

Source: realtor.com®

Search for your next home for FREE! Click below!

Laura Key

Realty Goddess

Laura Key on CBS News

Make Your Pad Reflect You

Hey men should know how to trick out their pads just as much as women do! I have a high amount of male clients who purchase homes, and they don't need Martha Stewart to make it their own! Ready to have your OWN space men? Call me! Laura Key 310.866.8422

Whether you're a sports buff or the trendy guy in your posse, we've got ways to make your pad part of your image.

By Karin Eldor, Fashion Correspondent

Page 1: Bachelor pad furniture

If you are where you live, what does that say about the maintenance and effort you have to put into your home? Well, that all depends on what you want others to think about you. So if you're decked out in expensive threads, your effort won't mean much if your place is a disaster, or worse, not a reflection of you.

Whether you live in a small apartment, a 1,500-square-foot condo or a three-level house, the home you call your own is your representative. And when a fine lady comes over to pay you a visit, you want to make sure she's impressed by your space.

You don't need to be an interior designer or spend tons of cash to be proud of your pad. As long as you feel comfortable in it, you will hold your head up high... even while lounging in your favorite chair.

who are you?

Start by asking yourself the following questions, for a self-inventory checklist:

How would you describe yourself? (athletic; cultured; ambitious; stylish; indifferent; etc.)

What are your hobbies? (mountain climbing; traveling; scuba diving; world history; wine tasting; golf; playing music; screenwriting; etc.)

These might seem obvious to you, but remember; making your home a reflection of you is worthless without knowing what your image is -- or at least what you want it to be.

No passions or traits have to be exclusive; you are likely an amalgamation of characteristics and that can be reflected in your home.

get started

The following are different broad categories that can be used as templates for decorating your pad, to bring out the "you" you're going for (based on your profile). Remember; you can be a combination of each of these categories.

The Athletic DudeWhether you're usually glued to the TV watching the big game (and this can mean several simultaneous games) or love reciting sports scores with your buddies after scoring big in your own football game, sports are your thing. Show your appreciation by adorning your home with things like vintage sports jerseys and mementos. And of course, you can't forget a widescreen plasma TV (50 inches or more) -- made larger than life with surround sound -- so that you can watch the game in style while sitting in a super cool recliner.

The HipsterWhen it comes to style, you've got it in spades -- at least that's what your friends tell you. You're a leader who always knows the trends before they hit the streets and your posse relies on you to dictate the latest fashion. This character trait could get pricey when it comes to your home, which is why I recommend starting with a classic, neutral base for the expensive items (i.e. couch, dining table, etc.) and decking your pad out with ultra-hip accessories like cool lamps, trendy vases, a stylin' coffee table, and cutting-edge gadgets.

Whether you're cultured or ambitious, here are some ideas for your home...

Page 2: Home decor

The Cultured BlokeThe ladies are always impressed by your appreciation for the finer things in life, be it your knowledge of fine wine, your travels to Botswana and Brussels, or your penchant for investing in valuable art. Make your pad your canvas by covering the walls with your favorite paintings, and rather than a table from Pottery Barn or Ikea, search for an antique table last used by Louis IVX. Store your wine collection in a slick wine cabinet and display your African masks in the living room.

The GourmetThere's nothing wrong with knowing your way around the kitchen; after all, you've been known to woo women with your creations. Show your female guests that you can satisfy their hunger (and more) by investing in a luxurious kitchen. If you enjoy spending time experimenting with food, make yourself more comfortable by installing a kitchen island, and treat yourself to an industrial-style stainless steel oven range. Pimp up your kitchen with a slick fridge or exhaust hoods, a rack to hang copper pots and pans over your oven or island, or, for those on a tighter budget, accessorize with appliances like a sleek toaster, blender and coffee maker.

The Zen Master Show off your inner peace by placing fresh bamboo or stones in clear glass vases, or for a bigger investment, treat yourself to a Jacuzzi with jets in your favorite bathroom. Maintain a minimalist look with white walls and furniture, and an overall sleek decor.

The WorkaholicWhile this might not be a character trait you want to flaunt, you can spin your workaholic tendencies as "ambitious." Set up a home office with a flat-screen computer, a state-of-the-art desk chair, and a slick table with a lot of organizational features to make you look like a guy who's always in control.

maximize your space

You don't need to overhaul your home to give it that unique touch that's "you." If you've been living in your home for a while and are already settled in, sometimes a slight reorganization can do the trick, as can a paint job and some new accessories.

Source: www.AskMen.com

Do you work from home? Buy your next home with your office in mind!

If you work from home, and it is time to move to your next home, there are some factors you should consider carefully before making your decision.

The flexibility afforded by a “zero-commute” combined with the skyrocketing price of gasoline has strengthened the case for full time teleworking and telecommuting. According to an Environmental Protection Agency (2004) study:

“Americans spend an average of 46 hours per year stuck in traffic. Gridlock produces more than $63 billion in congestion costs per year”

The artist community has been well acquainted with the use of work/living spaces for years, but improvements in technology have made the benefits of teleworking and occasional telecommuting more attractive to general consumers. According to the key findings form the International Telework Association & Council (ITAC) Telework America (2000) study:

“Home-based teleworkers also have larger homes, on average, than non-teleworkers; the difference amounting to about 500 square feet. The most popular place for an office in these larger homes is a spare bedroom, with the living room a distant second. The primary home telework activity is computer work (55% of total activities), followed by telephoning, reading, and—averaging 7% of the time—face to face meetings.”

As you purchase your next home, there are certain factors to consider if you need to set up a new home office:

Make sure that your high-tech needs can be met. Have a qualified electrician inspect the wiring of the house to see if the system can handle the extra power load that your home office requires. Older homes may need significant upgrades to handle the extra power, while newer homes are built with more energy-efficient systems to handle the additional power along with heating/air conditioning requirements. If you use cable, DSL or satellite internet access, check with your local service provider to see if access is available in your new neighborhood. Shop around for your telephone provider—in some cases, business service bundles may be more cost effective than regular residential service.

Designate where your office space will be. Determine the amount of space you will need to accommodate your work style and space. In many cases a spare bedroom or living room space can be used, if a formal den option is not available. If your work requires heavy telephone usage or just heads-down concentration, you may want to consider utilizing a room with a door. Doors can be closed to reduce interruptions from other family and household noises.

Plan your office blueprint to include all required furniture, bookcases, computers, fax, and printers. Make sure to allow for filing and storage space for files and extra office supplies. Lighting is critical for computer or assembly work, so make sure to allow for direct sunlight along with any specific task lighting that may be necessary. Select flooring options that will allow you to work comfortably—you may wish to go with hardwood or laminate flooring to allow for your chair to move smoothly across the floor. Install enough phone lines to cover your home, business and fax machines needs.

Is the office easily accessible? If you will expect regular package deliveries, make sure that your designated office is easily accessible to the front door of the home. This is also necessary if you will need to meet clients or visitors in your office and would like to ensure a professional appearance for your business.

Find out about local business requirements. Some cities have zoning restrictions and guidelines for work/living spaces along with tax implications. Make sure to check with your local government to determine if special restrictions exist.

Are you ready to find a home that could allow you to work from home? Or...do you need more room in the current home you own? Give me a call - lets get you started!

Bankruptcy And Buying A House - Is It Smart To Buy A House After Bankruptcy?

Each year, millions of people file bankruptcy as a means of erasing their consumer debts. While this approach may relieve stress, a bankruptcy is damaging, and will hang over your head for the next ten years. Still, it is possible to overcome bankruptcy. The key is making smarter financial and credit decisions. With this said, some people choose to purchase a home after a bankruptcy. Here are a few pointers to consider when buying a home.

Each year, millions of people file bankruptcy as a means of erasing their consumer debts. While this approach may relieve stress, a bankruptcy is damaging, and will hang over your head for the next ten years. Still, it is possible to overcome bankruptcy. The key is making smarter financial and credit decisions. With this said, some people choose to purchase a home after a bankruptcy. Here are a few pointers to consider when buying a home.

Reasons to Delay the Buying Process after Bankruptcy

If you consult with mortgage or financial experts, they will likely discourage you from buying a home following a bankruptcy. After your bankruptcy is discharged, there is a black cloud that looms over your credit report.

When any prospective lender reviews your report, they will be notified of your recent or past bankruptcy. In some instances, this justifies an immediate denial. On the other hand, there are lenders eager to help you establish or rebuild your credit. Thus, they will approve a loan request. Nonetheless, the penalties are steep.

Higher mortgage rates can be anticipated when purchasing a home after bankruptcy, especially if you have not established other credit accounts. Mortgage lenders consider two factors: credit scores and credit reports.

Although a bankruptcy appears on your credit report, having a high credit score will increase your odds of getting a comparable rate. Unfortunately, if you buy immediately following a bankruptcy, you will not have the opportunity to boost your score.

Reasons to Buy a Home after Bankruptcy

Lenders will approve mortgage loan applications one day following a discharge. Therefore, it is possible to get a home after a bankruptcy. Buying a home is perfect for rebuilding credit. Moreover, it is the quickest way to increase your credit score.

After a bankruptcy, the average person has a credit score below 600. Good credit consist of credit scores 650 and above. Maintaining current mortgage payments will gradually increase your score. After two years of regular payments, you will have established a good payment history. Hence, you may qualify for a low rate refinancing, which may lower your mortgage payments.

Ready to search for your new home? Start here!